Moving Containers

Recommendation

Moving Container Reviews

Recommendation

Truck Rentals Reviews

Storage Recommendations

Storage Review

Junk Removal Recommendations

Junk Removal Reviews

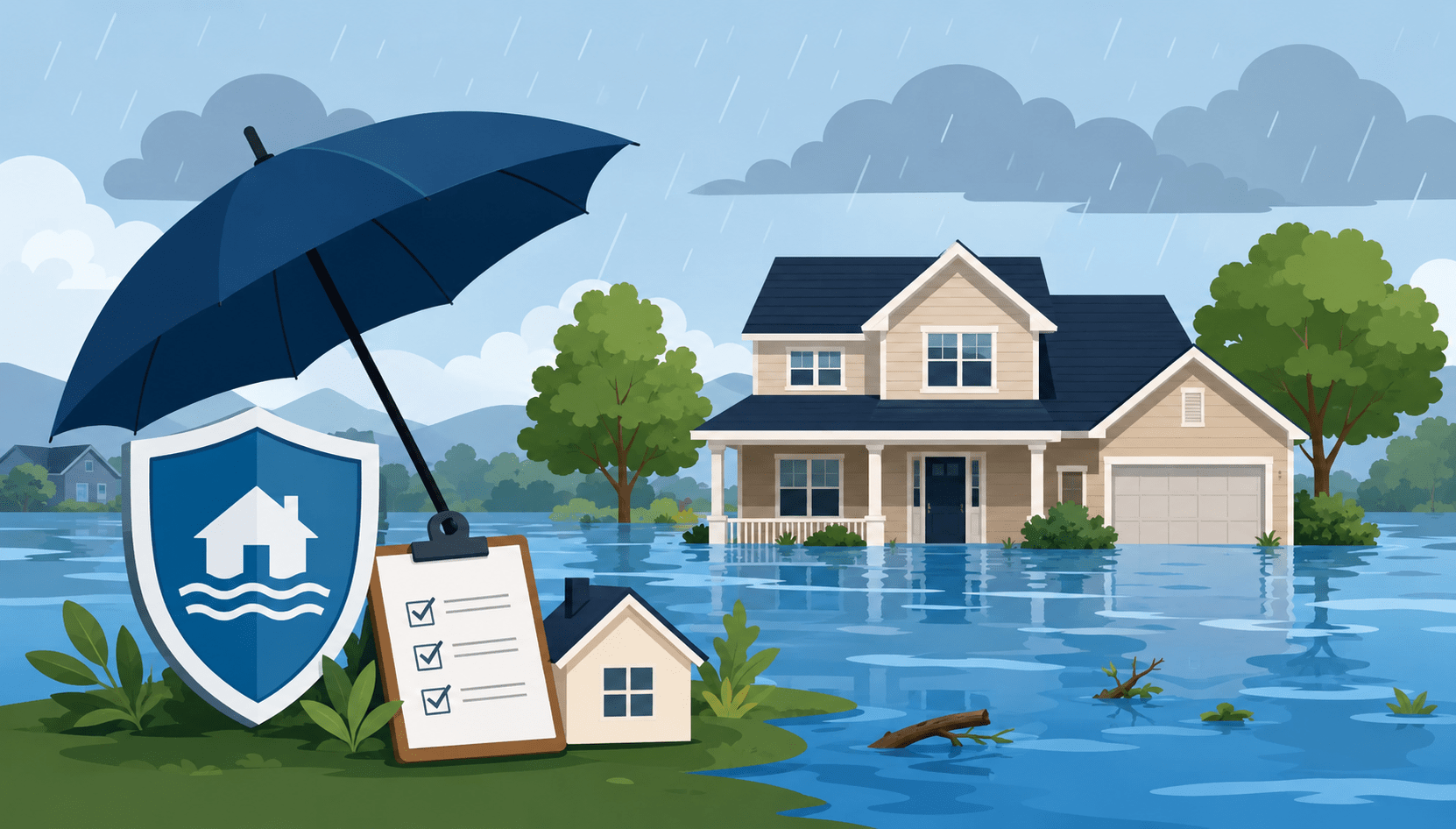

Moving into a new home comes with plenty of decisions, from choosing the right neighborhood to protecting your investment after closing day. One detail many buyers overlook until the last minute is flood insurance. If you’re purchasing a property in a flood-prone area, your lender may require it before approving your mortgage. Even if it’s not mandatory, flood insurance can still play a major role in protecting your finances and belongings.

Understanding how flood insurance works, what it covers, and when you need it can help you avoid expensive surprises later. Whether you’re relocating across the country or settling into a coastal community, knowing how flood protection fits into homeownership is essential when purchasing a new property before relocating.

Flood insurance is a specialized insurance policy designed to cover damage caused by flooding. Standard homeowners insurance policies typically do not cover flood-related losses, which means homeowners must purchase separate flood coverage if they want financial protection against water damage caused by natural flooding events.

Flooding can happen almost anywhere. Heavy rain, hurricanes, overflowing rivers, storm surges, melting snow, or drainage system failures can all cause severe water damage. Even homes located outside officially designated flood zones can experience flooding under the right conditions.

Flood insurance policies are commonly backed by the National Flood Insurance Program (NFIP), which is managed by FEMA. Some private insurance companies also offer flood insurance policies with expanded coverage options.

When buying a home, lenders evaluate whether the property is located in a high-risk flood zone. If it is, flood insurance is often required before the mortgage can close.

Many homeowners assume flooding only affects beachfront or riverside properties. In reality, flood damage is one of the most common and costly natural disasters in the United States.

Even a small amount of standing water can create thousands of dollars in repair costs. According to FEMA estimates, just one inch of floodwater inside a home can cause around $25,000 in damage.

That’s why flood insurance should be part of your relocation planning process, especially when moving into an unfamiliar area. Before finalizing your move, it’s important to understand regional weather risks, drainage conditions, and property history.

At the same time, protecting your belongings during relocation is equally important to avoid unexpected losses while transporting valuables.

Flood insurance policies generally include two separate forms of protection:

This portion covers the physical structure of your home and permanently installed systems.

This covers belongings inside the home, including furniture, clothing, electronics, and appliances.

Most NFIP policies provide coverage limits up to:

$250,000 for building property

$100,000 for personal belongings

Private insurers may offer higher coverage limits and additional options depending on the property and location.

Unlike standard home insurance claims, flood insurance policies specifically define what qualifies as a flood event. Generally, flooding must involve water affecting at least two properties or two acres of land.

One of the first things buyers should do before closing on a property is determine the home’s flood risk level.

Mortgage lenders typically use FEMA flood maps to identify whether the home falls inside a Special Flood Hazard Area (SFHA). If it does, flood insurance may be legally required for federally backed loans.

However, living outside a high-risk zone does not eliminate the possibility of flooding. In fact, a significant percentage of flood claims come from properties located in moderate- or low-risk areas.

You should strongly consider flood insurance if the property:

Is near rivers, lakes, or coastal areas

Has poor drainage infrastructure nearby

Is located in a hurricane or storm-prone region

Has a history of flooding

Sits at a lower elevation than surrounding homes

During the buying process, ask your real estate agent about prior flood claims and neighborhood flood history. Reviewing local flood maps and inspection reports can also provide useful insights.

Flood insurance policies can vary slightly, but most provide protection for both the home structure and personal belongings.

Personal contents coverage usually includes:

Clothing and personal items

Furniture and curtains

Electronics and gadgets

Portable air conditioners

Microwaves

Washers and dryers

Freezers and food stored inside freezers

Valuable items up to policy limits

Non-installed carpets and rugs

This coverage helps replace damaged belongings after a covered flooding event.

Building coverage generally protects:

The home’s foundation and structure

Electrical systems

Plumbing systems

HVAC systems

Water heaters and furnaces

Refrigerators and cooking appliances

Permanently installed cabinets and bookshelves

Built-in carpeting

Window blinds

Detached garages

Debris removal

Coverage applies to repairs directly related to flood damage.

Flood insurance has limitations that homeowners should understand before purchasing a policy.

Most flood insurance policies do not cover:

Temporary housing expenses

Landscaping damage

Swimming pools and patios

Cash or financial documents

Vehicles

Mold damage caused by neglect

Sewer backups unrelated to flooding

Certain basement items may also have limited coverage.

Understanding exclusions is critical because many homeowners mistakenly assume all water-related damage is automatically covered.

Flood insurance coverage in basements and crawl spaces is often more restricted than coverage for above-ground living areas.

Typically covered items include:

Foundation walls

Electrical outlets

Fuel tanks

Air conditioning systems

Furnaces

Water heaters

Drywall in unfinished areas

Personal belongings stored in basements may not receive the same level of reimbursement as items located in primary living spaces.

Because of these restrictions, homeowners in flood-prone regions often avoid storing valuable possessions below ground level.

Many buyers confuse flood insurance with traditional homeowners insurance, but they serve very different purposes.

Standard homeowners insurance typically covers:

Fire damage

Theft

Windstorms

Liability claims

Certain types of water damage

Flood insurance specifically covers rising water caused by natural flooding events.

For example:

A burst pipe inside your home may be covered by homeowners insurance.

Water entering your home due to heavy rainfall and street flooding would generally require flood insurance coverage.

Having both policies creates stronger protection for homeowners in vulnerable regions.

Flood insurance premiums vary based on several factors, including:

Property location

Flood zone classification

Elevation

Home age and structure

Coverage amount

Deductible selection

Homes in high-risk areas usually carry higher premiums. However, homes outside major flood zones may qualify for relatively affordable coverage.

Private insurers sometimes offer competitive pricing or expanded protection beyond NFIP limits.

When budgeting for a move, insurance expenses should be considered alongside closing costs, inspections, utility setup fees, and moving services.

Flood insurance policies often include waiting periods before coverage becomes active.

NFIP policies commonly have a 30-day waiting period unless coverage is required for a mortgage closing.

This means homeowners should not wait until storm season begins to purchase protection. Planning early helps avoid gaps in coverage.

If you’re relocating during hurricane season or moving into a coastal state, arranging flood insurance ahead of time is especially important.

Flooding risks are becoming more common due to changing weather patterns, urban development, and aging drainage systems.

Areas previously considered low-risk are now experiencing flash floods and unexpected storm damage. Increased rainfall intensity and expanding paved surfaces contribute to water runoff problems in many suburban communities.

Because flood patterns continue evolving, homeowners should reassess insurance needs regularly rather than relying solely on historic flood maps.

If you’re purchasing your first home, these practical steps can help simplify the process:

Understanding your property’s flood designation helps estimate both risk and insurance costs.

Sellers may disclose prior flooding incidents or water damage history.

Private insurers sometimes offer broader protection or higher limits.

Lower premiums often come with higher out-of-pocket costs during claims.

Documenting personal items makes the claims process easier after a disaster.

Insurance is only one part of flood preparedness. Homeowners can also reduce risk through preventive improvements.

Consider:

Installing sump pumps

Elevating utilities

Improving yard drainage

Sealing foundation cracks

Using flood-resistant building materials

If you’re relocating into a flood-prone property, taking preventive measures early can significantly reduce future repair costs.

You should also confirm that your movers carry adequate protection before transporting expensive belongings to prevent costly moving-related issues before settling into your new home.

Once you move in, your focus naturally shifts toward creating a comfortable living space. Homeowners relocating into flood-prone areas often prioritize practical upgrades alongside interior design improvements.

Simple adjustments like elevated furniture placement, moisture-resistant flooring, and strategic storage solutions can help minimize future flood damage while improving day-to-day living.

At the same time, many homeowners begin planning layout improvements and décor updates immediately after unpacking.

No. Flood insurance is usually only mandatory for homes located in high-risk flood zones with federally backed mortgages. However, any homeowner can purchase coverage voluntarily.

Standard renters insurance generally does not cover flood-related losses. Renters may need separate flood insurance for personal belongings.

Most standard flood insurance policies do not cover additional living expenses or temporary housing after displacement.

Flood insurance policies are typically renewed annually.

Coverage usually does not begin immediately. Most policies have waiting periods, so purchasing coverage early is important.

Yes. Many flood claims come from moderate- and low-risk locations. Even minimal flood damage can create significant repair expenses.

Flood insurance is one of the most overlooked parts of buying a home, yet it can become one of the most valuable protections a homeowner has. Whether coverage is required by your lender or purchased voluntarily, understanding what flood insurance covers helps you make smarter financial decisions during a move.

Flooding can happen unexpectedly, even outside designated flood zones. Taking time to review risks, compare policies, and prepare your home properly can save thousands of dollars in future damage and repairs.

For anyone relocating into a new property, flood insurance should be considered part of a complete home protection strategy — alongside moving insurance, property inspections, and long-term maintenance planning.