Moving Containers

Recommendation

Moving Container Reviews

Recommendation

Truck Rentals Reviews

Storage Recommendations

Storage Review

Junk Removal Recommendations

Junk Removal Reviews

Relocating for a new job used to come with at least one financial upside: the possibility of writing off certain moving-related costs on your taxes. But recent changes to federal tax laws have reshaped what workers can and cannot deduct when moving for employment opportunities. If you’re planning a relocation in 2026, understanding how these tax updates work could save you from expensive surprises.

From transportation and temporary housing to hiring professional movers, relocation costs can add up quickly. At the same time, many Americans are reconsidering where they live due to career shifts, remote work flexibility, and changing living expenses. In fact, understanding why americans move so often ,helps explain why relocation-related tax questions are more relevant than ever.

This guide breaks down the latest rules around deductible relocation costs, who still qualifies, and how to plan your move strategically in today’s tax environment.

The tax treatment of relocation costs changed significantly after the Tax Cuts and Jobs Act (TCJA). Before that legislation, many taxpayers could deduct qualifying relocation expenses if they met distance and employment tests.

Today, most civilians can no longer claim relocation write-offs on their federal tax returns. The deduction suspension remains active through 2025 and may continue depending on future legislation.

However, there are still a few important exceptions.

Currently, only active-duty military members moving under official military orders can generally qualify for federal relocation deductions.

For everyone else, relocation expenses tied to employment are usually considered personal expenses rather than deductible business costs.

That means if you’re moving for a new corporate role, hybrid position, or remote opportunity, the IRS likely will not allow you to write off your moving costs on your federal return.

Lawmakers introduced these restrictions as part of a broader effort to simplify itemized deductions and offset corporate tax reductions. While supporters argued the changes streamlined tax filing, critics noted that employees relocating for work lost an important financial benefit.

This shift has had a noticeable impact on professionals accepting out-of-state job offers. Many workers now negotiate relocation assistance directly with employers instead of relying on tax relief later.

At the same time, inflation is driving up moving costs, making relocation more expensive than ever for households already navigating rising rent, fuel, and labor expenses.

Under the current federal rules, most taxpayers cannot deduct common relocation-related expenses, including:

These limitations apply even if the move is mandatory for a new employer.

Many people still search for a valid moving expenses tax deduction, but unless they meet a qualifying military exception, those claims are generally unavailable at the federal level.

Yes, in most cases.

If your employer reimburses you for moving costs, those payments are usually treated as taxable income. This means reimbursement funds may appear on your W-2 and increase your taxable earnings.

Employer-covered benefits that may count as taxable compensation include:

Some companies choose to “gross up” relocation packages to help offset employee tax burdens, but not all employers offer this benefit.

Before accepting a relocation package, ask HR whether reimbursements will be taxed and how they’ll appear on payroll records.

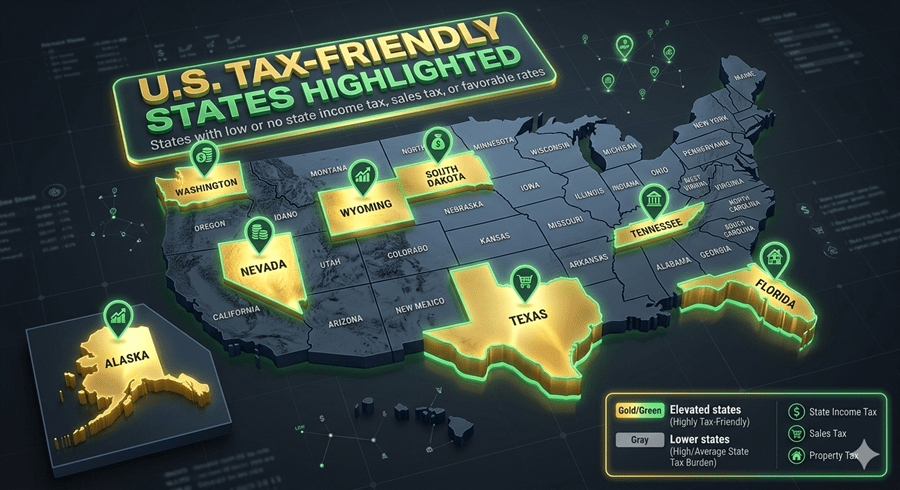

While federal deductions are mostly unavailable, some states still provide limited tax relief for certain relocation-related situations.

Because state laws vary widely, it’s important to research the tax structure of your destination before moving.

For example, individuals relocating south often compare new jersey to florida tax differences when evaluating long-term financial savings tied to income tax policies.

Some states offer advantages such as:

These differences can significantly affect the true cost of relocating for work.

A job-related move can influence much more than your address. It may affect:

Workers moving mid-year sometimes need to file multiple state tax returns depending on residency periods and income sourcing.

Understanding your broader moving tax situation before relocating can help avoid unexpected liabilities during filing season.

Because tax deductions are now limited, workers should prepare for higher out-of-pocket relocation expenses.

Fuel, flights, vehicle shipping, tolls, and hotels can create substantial expenses during long-distance moves.

Security deposits, utility activation fees, and advance rent payments often create large upfront costs.

Hiring experienced movers remains one of the largest relocation expenses for many households. Comparing multiple moving company quotes can help reduce unnecessary spending while improving service transparency.

If you’re moving across state lines, researching the best interstate moving companies can help you avoid unreliable carriers and hidden fees.

Generally, no.

Even self-employed individuals typically cannot deduct personal relocation costs simply because they operate remotely or run a business from home.

However, some business-related transportation or equipment-moving costs may qualify as operational expenses under separate tax rules. Because these situations are highly specific, professional tax guidance is recommended.

Remote and hybrid work arrangements dramatically changed relocation patterns in recent years.

Employees are increasingly moving based on lifestyle preferences rather than office proximity. Lower living costs, warmer climates, and tax-friendly states have become major drivers of migration.

This trend also changed how companies structure relocation assistance. Instead of traditional corporate transfers, many employers now offer flexible relocation stipends or remote transition packages.

Without broad federal deductions available, strategic planning matters more than ever.

Include both obvious and hidden costs, such as:

Some employers cover only transportation, while others include housing support or lump-sum relocation payments.

Clarify whether benefits are taxable before signing employment agreements.

A higher salary does not always mean improved financial stability.

Evaluate housing, insurance, transportation, and taxes when comparing relocation destinations.

Income changes tied to a new position may also affect your federal bracket exposure under the evolving 2026 tax brackets landscape.

Tax policies can change quickly depending on future legislation and economic priorities.

Some lawmakers have proposed restoring deductions for work-related relocation expenses, especially as labor mobility remains important in competitive industries.

However, there is currently no guaranteed timeline for major federal changes.

Employees considering relocation should make decisions based on existing rules rather than assuming future deductions will return.

Retirees who relocate closer to family or to lower-cost states often wonder whether any deductions still apply.

Although most federal relocation write-offs remain unavailable, retirees should still evaluate how a move impacts retirement income taxation, healthcare access, and estate planning.

Some individuals researching a potential moving tax deduction for seniors may discover state-level exemptions or retirement tax benefits that create meaningful long-term savings.

Since most workers can no longer rely on federal deductions, reducing expenses upfront becomes more important.

Selling or donating unused items can lower transportation costs substantially.

Summer is often the most expensive moving season. Scheduling during fall or winter may reduce rates.

Never accept the first estimate you receive. Comparing pricing, reviews, and insurance coverage helps avoid overpriced services.

Employers may be willing to increase signing bonuses or relocation assistance if deductions are unavailable.

The tax landscape for relocation has changed dramatically over the past several years. For most workers, job-related moving costs are no longer deductible at the federal level, even when relocating is necessary for career advancement.

That makes preparation more important than ever. Understanding taxable relocation reimbursements, researching state tax differences, and budgeting carefully can help minimize financial stress during a move.

As relocation trends continue evolving alongside remote work and economic shifts, workers who plan proactively will be in the best position to manage both the logistical and financial side of moving successfully.

Most taxpayers currently cannot deduct job-related moving expenses on federal returns.

Yes, most relocation reimbursements are considered taxable income.

Some states offer limited relocation-related tax benefits depending on local laws.

Generally, remote employees cannot deduct personal relocation expenses.

Yes, qualifying active-duty military moves may still receive federal tax deductions.